, a subcohort of size

, a subcohort of size  is obtained by simple random

sampling.

is obtained by simple random

sampling.The likelihood equations for case-cohort data were taken from

the original paper by Prentice (1986) in which he proposed the case-cohort

design. From a cohort of size , a subcohort of size is obtained by simple random

sampling.

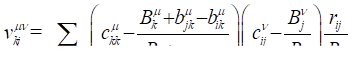

The quantities  ,

,  , and

, and  are as defined above. As given

by Prentice, the estimates of the relative risk are obtained from the

pseudo-likelihood, namely,

are as defined above. As given

by Prentice, the estimates of the relative risk are obtained from the

pseudo-likelihood, namely,

(A.4)

(A.4)

where  is now the set of all members of

the risk set who are also in the subcohort sample and the case at

is now the set of all members of

the risk set who are also in the subcohort sample and the case at  . differs from

. differs from  , which was a set of all members

of the risk set.

, which was a set of all members

of the risk set.

The likelihood is the product over all  subjects in the cohort; factors

in expression 8.4 may differ from one only for cases and members of

subjects in the cohort; factors

in expression 8.4 may differ from one only for cases and members of  . This implies that, although only the

covariate vector

. This implies that, although only the

covariate vector  for cases and the subcohort are

directly used in parameter estimation, the full cohort must be followed to

determine

for cases and the subcohort are

directly used in parameter estimation, the full cohort must be followed to

determine  and, in particular,

and, in particular,  .

.

The maximum pseudo-likelihood estimate,  , for

, for  is the quantity that nullifies

the

is the quantity that nullifies

the  partial derivatives of the

logarithm pseudo-likelihood, namely,

partial derivatives of the

logarithm pseudo-likelihood, namely,

(8.5)

(8.5)

where

Using a Taylor's series expansion, a consistent estimate of the

covariance matrix for  is given by the so-called

“sandwich” estimator

is given by the so-called

“sandwich” estimator

, where

, where  is the matrix of mixed partial

derivatives of the log likelihood

is the matrix of mixed partial

derivatives of the log likelihood  and is the covariance matrix of

and is the covariance matrix of

at

at  .

.

In place of the matrix of mixed partial derivatives, PEANUTS

uses the more easily computed quantity obtained from expression 3 with  replacing

replacing  .

.

The covariance matrix of requires extensive calculations

because of . The  element of is given by

element of is given by

(A.6)

(A.6)

Since the pseudo-likelihood conditions on noncensored failure

times, we have  for all censored

for all censored  failure times, that is, with

failure times, that is, with  .

.

For each noncensored failure time,  with

with  , the element of the covariance matrix

of

, the element of the covariance matrix

of  is given by the usual

expectation of

is given by the usual

expectation of  , namely,

, namely,

where

and

Next, let  be an indicator

function that takes value 1 if the failure at time occurs outside the subcohort and

value 0 otherwise. Suppose

be an indicator

function that takes value 1 if the failure at time occurs outside the subcohort and

value 0 otherwise. Suppose  with the case occurring within the

subcohort,

with the case occurring within the

subcohort,  . Then , since

. Then , since  is fixed, because the risk set

at ,

is fixed, because the risk set

at ,  , consists only of subcohort members

and, conditional on all covariate and censoring histories up to ,

, consists only of subcohort members

and, conditional on all covariate and censoring histories up to ,  can be fully characterized. With

can be fully characterized. With

=1, conditioning on covariate

and censoring histories and the observed exposures at , we cannot know for certain which of

the

=1, conditioning on covariate

and censoring histories and the observed exposures at , we cannot know for certain which of

the  members is the case and

therefore not in the subcohort, and thus we cannot know the composition of

members is the case and

therefore not in the subcohort, and thus we cannot know the composition of  . This randomness induces the

covariance between and

. This randomness induces the

covariance between and  . Prentice specifies the covariance as

. Prentice specifies the covariance as

A similar expression is obtained for  . Note that because of differences in

the composition of and and possible covariate changes

over time,

. Note that because of differences in

the composition of and and possible covariate changes

over time,  may not equal .

may not equal .

Expression 7 can then be rewritten as

In the case of ties in the failure times of noncensored cases, Prentice suggests modifying the likelihood using the methods given by Peto (1972) and Breslow (1974) for the partial likelihood, namely,

where  is the number of ties.

is the number of ties.

The subcohort is selected at the start of follow-up. One possible disadvantage of the case-cohort approach occurs when there is substantial censoring; there may be no members of the subcohort to compare with later-occurring cases. Prentice (1986) and others have suggested that this problem can be minimized by sampling one or more additional subcohorts. Because the covariance between scores depends on the sampling, the equations provided above are not valid for all types of repeated subcohort sampling schemes. However, the formulae are valid for the important special cases where the subsequent subcohort is a simple random sample from the remaining cohort; in particular, the formulae are valid when a subsequent subcohort includes all remaining cohort members. Members of a new sample are “entered” through the use of a late entry (or left-truncation) variable with the EPICURE command ENTRY varname @. The estimated baseline survival curve (see below) is valid only if the sampling fraction is the same for all subcohort selections.

In his paper, Prentice also suggests a natural estimator for the cumulative baseline hazard function, from which an estimated baseline survival curve can be obtained by exponentiating the negative cumulative hazard. The form of the estimator for the cumulative hazard is the same as for a full cohort, but it is modified by division by the sampling fraction. If a survival plot is requested in EPICURE with the SCURV command, then the sampling fraction must have been provided in a previous CSCHRT fraction @ command.

The smoothing algorithm for the survival curves is implemented with the SCURV command; adjustments to the curves are made using the subcohort sampling fraction.